Written by Muqi Wulan

The material provides the basic information on cost estimation at Level 1.

It is widely recognised that over 70% of the final product costs are determined during design (Boothroyd, Dewhurst & Knight 2011: 7), as illustrated in Figure 1. The majority of costs have been committed when the principle solution has been selected in the conceptual and embodiment design. Relatively, there are very limited chances to reduce costs at the stages of production and assembly. It is important, therefore, to identify cost elements or factors, and start cost estimation as early and accurately as possible in the design process since later design changes can result in considerable increase of manufacturing cost. Although any iteration and improvement may prolong the design process, it is still more economical than making changes at the stage of production (Pahl et al 2007: 535).

Figure 1 – Who casts the biggest shadow? (Munro and Associates, Inc. 2009)

Factors of overall product cost

Costs are classified in different ways based on their relationship to the production volume and manufacturing operations (Pahl et al 2007: 535) (Dieter & Schmidt 2009: 780) (El Wakil 1998: 415). The overall cost of a product can be divided into two major categories.

• Direct costs, which can be allocated directly to a specific cost carrier and associated with a particular unit of product, for example material and labour costs.

• Indirect costs, which can not be allocated directly or identified with any particular products, for example, running a shop and cost of utilities.

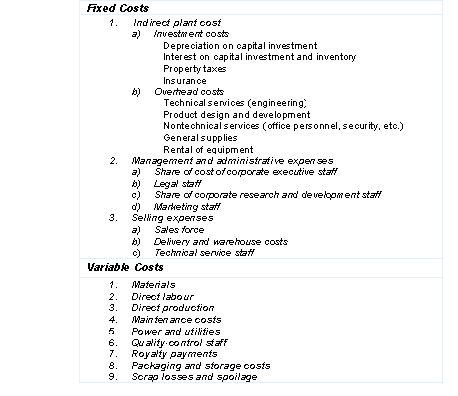

Another way to classify costs as fixed costs and variable costs. Table 1 lists the factors in these categories.

• Fixed costs, which are independent of the production volume.

• Variable costs, which depend on the production volume, for example, the order number of items, the degree of facility utilisation or the batch size.

Table 1 – Factors in fixed and variable costs (Dieter & Schmidt 2009: 780)

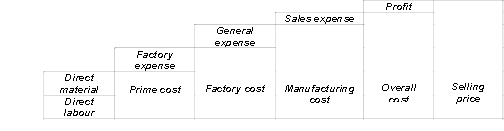

Figure 2 shows the way the elements of cost build up to contribute the overall cost of a product and its selling price.

Figure 2 – Elements contributing to the overall cost of a product (Dieter & Schmidt 2009: 782)

Calculations on prime cost

Here a brief description is given on more precise cost calculations on the prime cost (shown in Figure 1.2) – the variable part in manufacturing cost of a product (VMfC). It consists of direct material costs (DMtC) and production labour costs (PLC) including assembly costs. All costs for production and assembly operations have to be added (Pahl et al 2007: 537).

VMfC = DMtC + PLC (1)

The direct material costs are determined by the weight W or volume V and the specific cost c, which is cost per unit weight or volume, as follows:

DMtC = cw x W = cv x V (2)

The direct production labour costs can be calculated from the time needed for the individual production processes and assembly operations multiplied by a labour cost factor cL.

PLC = cL x (tp + ts +tsu) (3)

where tp is the primary time, ts is the secondary time, and tsu is the set-up time including distribution and recovery time.

Summary

Early cost estimation in design is critical to meet the requirement in product cost. The overall product cost can be generally divided into direct and indirect costs, or fixed and variable costs.

References

Boothroyd, G., Dewhurst, P., Knight, W. A. (2011) Product design for manufacture and assembly. 3rd edn. Boca Raton: CRC Press, Taylor & Francis Group

Dieter, G.E., Schmidt, L.C. (2009) Engineering design, 4th edn. New York: McGraw-Hill

El Wakil, S. D. (1998) Processes and design for manufacturing. 2nd edn. Boston: PWS Publishing Company

Munro and Associates, Inc. (2009) The design determines the cost. [online] available from [02 September 2011]

Pahl, G., Beitz, W., Feldhusen, J. and Grote, K. H. (2007) Engineering design: a systematic approach. 3rd edn. London: Springer

Back to Detail Design

Back to MAE Design Model